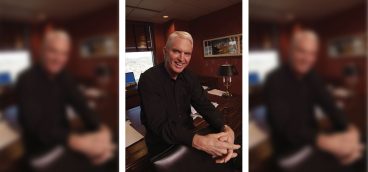

What Do I Know? Stanley Druckenmiller

I was born in 1953 in Philadelphia and grew up in New Jersey and Virginia. By the eighth grade, I had attended six public schools before being enrolled at a private day school in the ninth grade.

My father, who was a chemistry major in college, worked for Dupont and ended up in labor relations. When I was 9, he was transferred to the company’s Textile Fibers Department in Richmond, Virginia, and subsequently was transferred to Wilmington, Delaware, after my junior year in high school. When my father was transferred again, right before my senior year, four local families were kind enough to put me up for two or three months apiece so that I could graduate with my class at Collegiate School in Richmond. I don’t know how all the moving around affected me, other than I have no memory of any time before high school.

My parents were good but overprotective. And I always had an awkward relationship with my mother. When I was in elementary school, my parents got divorced because my mother had an affair. Rightly or wrongly, she considered herself at fault for the breakup of the marriage and feared that she would, as a result, lose custody of me and my two sisters. My father was also afraid that he would lose us because, even today, custody customarily goes to the mother. So, my parents decided to “split the baby,” so to speak. My sisters went to live with my mother in New Jersey, and I was raised by my father from the age of 6, first in New Jersey, and then in Richmond, until he married my stepmother two years later.

My stepmother did a fantastic job of parenting, although I did get to spend a month every summer with my mother and sisters. I didn’t think too much about it at the time, but I came to understand later just how weird it was that my parents chose to divvy up their kids. It bothered me but, over time, things worked out. My sisters are doing well, and we’re all happy and have families. Parenting books say that our situation was not good, but reality told me otherwise. That experience may have driven me to reach for success on my own.

In 1971, I enrolled at Bowdoin College in Maine as an English major, and soon realized that I couldn’t compete with the other kids in the program. But during my junior year, I learned that I was competitive in economics and gained confidence from that. So, I graduated from Bowdoin in 1975 with a bachelor of arts degree in English and economics.

As an undergraduate, I met the woman from Pittsburgh who would become my first wife. She had one year left at Bowdoin after I graduated, and I was accepted into the University of Michigan’s Ph.D. program in economics. It only took a semester-and-a-half for me to realize that graduate economics was not for me, and I dropped out toward the end of my second semester. I subsequently got married and moved to Pittsburgh with my new wife. I was 22 years old, and after a few months, we knew our marriage wasn’t going to work, but my love of Pittsburgh endured.

The first day I was there was on a Saturday night in 1975, the day before the AFC Championship Game when the Steelers beat the Raiders; they went on to win their second Super Bowl. I had interviews scheduled at Pittsburgh National Bank and Mellon Bank, the latter of which I flunked and got no job offer. But Tom O’Brien, who was the head of commercial lending at Pittsburgh National at the time, took a chance and hired me.

I started in the management training program in 1976 and soon learned that, at the bank, the common road to success was through commercial lending, which went through the Credit Department. One day, the head of Credit called and explained to me that commercial lending was about relationships and selling. He said, “You couldn’t sell a snowmobile in Alaska if there was no other form of transportation,” so I knew that I wouldn’t have success in commercial lending. But there was a man named Speros “Doc” Drelles up on the 30th floor who handled investments for the Trust Department. His work was more about numbers and performance. Drelles took me under his wing and became my mentor. Things went well from there.

By the time I was 25, Doc had promoted me into a significant position at Pittsburgh National. Most of the people reporting to me were in their late 30s and had MBAs, which I did not have. So, Doc took a real risk. And if you’ve ever read the book “Outliers,” I had served my 10,000 hours in a leadership position by the time I was 28, which was really an amazing gift to be given in this business. I had the energy of a 20-something, but the experience of someone in their late 30s. I was very lucky, and everything fell into place just right.

In truth, while not always confident, I was an extremely competitive person. I like winning, probably a little too much, to a fault. But the wonderful thing about the business in which I found myself is that every event affects a security price somewhere, and this has forced me to stay up to date on the latest trends and what’s happening in the world. I don’t think I could have survived in this business if I were doing it just for the money. Every day I had to compete against people who loved the work and would try to outwork me. But no one ever outworked me, and it isn’t because I have a great work ethic. It’s because I love my business as much or more than the next guy, so much so that it has never felt like work to me.

In February 1981, while still at Pittsburgh National Bank, I started my own investment firm, Duquesne Capital, with just two clients and only $800,000 under management. Charging 1 percent, this didn’t do much for us on the revenue side. Fortunately, there was one investor who paid me $10,000 per month just to talk to him and offer him ideas. In essence, he provided the revenue that kept us going.

One day, I mentioned to this man how much I loved bonds and, apparently, he took my advice a little too much to heart. He bought something like $8 billion worth, with no capital, and lied to Chase Bank and the depository trust company about the capital behind his investment. Then, one morning, I woke up to a Wall Street Journal article reporting that this same investor was going to jail because he had defrauded Chase Bank of $254 million. As a result, I lost the steady revenue stream that was covering Duquesne’s rent and expenses, and the firm was reduced to just me and an assistant. As you can imagine, I worked very hard and, from February 1981 to ’85, my return was 42 percent per annum. I don’t know if people believed it, or whether they just didn’t trust someone at such a young age. In any event, I couldn’t attract enough new clients to move Duquesne Capital forward.

Before too long, the man who was running Dreyfus, an American investment management company, offered me a portfolio management position and I took it. But one of the smartest things I ever did was, when he tried to buy Duquesne Capital, I refused to sell it. So, I ended up commuting from Pittsburgh to New York and back again and had great success for the year or two I was at Dreyfus. It was a relief moving to New York full time in 1986 when I was named manager of the Fund of Dreyfus and three others as part of my agreement with the firm. At the same time, I maintained management of Duquesne Capital.

At Dreyfus, I did well during the market crash of 1987, which made me more well known. Then one day, quite unexpectedly, someone at Dreyfus asked me, “Would you like to meet George Soros?” I answered with an enthusiastic “Yes!”

Meeting George Soros was helpful to me because, somehow, we had come to the same investment philosophy (though he was the first to invent it), which was to hold a large group of stocks long, a group of stocks short, and use leverage to trade bonds, futures and currency. No one else was doing business this way back then, which was basically investing not just in equities, but in bonds and currencies, commodities and credit — anything that moved. Soros had a significant impact on me. I started talking to him two weeks before the ’87 crash when, like an idiot, I went long on Friday afternoon, right before the crash happened. But over the weekend, I realized my mistake and, somehow, danced out of my problem by Wednesday. Duquesne ended the year up 99 percent.

Soros and I talked constantly and formed a bond. Before long, he offered me a job, and it took me a year to say “Yes” in 1988. Now, I’m a center-right guy — leaning very right on economics — and somewhat center-left regarding social issues. But with Soros, if you had a spectrum of 100 to the right, he’d be 100 to the left, so he and I had very different causes that we wanted to support. But I did pick up from him the culture and joy of philanthropy. It’s true that Soros has been a lightning rod when it comes to his political views and his funding of left-wing causes. But he’s had the money to make things happen in many places.

Also in 1988, at the age of 35, I got married again, to Fiona Katharine Biggs, and the second time was a charm. She has been a great partner to me for 36 years and a wonderful mother to our three children. My mother-in-law liked to say that I was an “idiot savant.” I wasn’t the smartest kid in my class in high school or college. But, somehow, I was gifted in one area: I knew instinctively how to compound money, which has been a huge part of my success, and one of the reasons that I am grateful and happy today. Earned success is fun, and contributing to important causes is fun, too.

When I consider many philanthropists I know, part of the reason they give is to feed their own egos and to wallow in the recognition that comes from it. But when I think of George Soros, he didn’t give for those reasons. He knew that some people didn’t like what he supported, but he didn’t care. And he never asked me or anyone else for money to fund any of his causes. He did it on his own.

I left Soros in 2000 and, for another 10 or so years, Duquesne Capital’s funds kept growing. That’s the power of compounding. But in 2010, I told my investors that I’ve been worn down by the stress of trying to maintain one of the best trading records in the industry, while managing an enormous amount of capital. So, I closed Duquesne; at that time, we had more than $12 billion in assets and were posting an average annual return of 30 percent, without a single losing year.

Over time, I had come to realize that my management style was not conducive to handling the kind of numbers that I could have managed at the Quantum Fund for George Soros. I’d rather make 30 percent per year with a smaller fund than be at the top of the heap of $100 billion at 8 percent, even though I’d make more money with the associated fees. And it’s not that I’m such a good person. I like performing, and I never wanted to have huge assets under management. I wanted to have the best returns in the industry.

As I’ve said, politically, I’m center-right, certainly on economic issues, and center-left when it comes to most social concerns. But giving large sums of money to political candidates, given what I think of most of them, doesn’t really do it for me. But giving money and watching, for example, the Harlem Children’s Zone become what it has become does a lot.

If you’re a philanthropist, supporting a person like Geoff Canada, a fellow Bowdoin College alumnus, is the key to success. Geoff founded the Harlem Children’s Zone (HCZ) in 2002, a world-renowned education and poverty-fighting organization based in New York City, and he has delivered. Today, I’m excited about the HCZ’s collaboration with Blue Meridian, a partnership of results-oriented philanthropists seeking to transform the life trajectories of our nation’s young people and families. The best way to describe the collaboration is “Harlem Children’s Zone 10.0.” In many places around the country, the HCZ has engaged with Blue Meridian to help scale up leaders of communities in defined geographic locations to create long-term and successful approaches to local issues that will help them not only to survive, but to thrive. This is very exciting to me.

As with my business, when it comes to my philanthropy, I make big, concentrated bets. Fiona and I channel roughly 95 percent of our giving into five or six institutions whose work we really care about. For example, we give to Memorial Sloan-Kettering and seeing the advances the Cancer Center has made to improve cancer outcomes for people is impressive and thrilling.

I joined the Sloan Kettering Board of Directors 28 years ago and, for the first 10 years, it was a real slog. The preferred method for treating cancer was to give patients a lot of chemotherapy and hope that it would kill the cancer before it killed them. Then, around 2005, through genetic sequencing — which tells scientists the kind of genetic information that is carried in a particular DNA segment — doctors realized that cancer is a personalized disease. Now, by harnessing the additional power of immunotherapy and AI (artificial intelligence), cancer is going to become a managed disease within the next 10 years.

In 2008, NYU Medical Center, as the institution was then known, was renamed the NYU Elaine A. and Kenneth G. Langone Medical Center in honor of its chair of the Board of Trustees and his wife, whose total unrestricted gifts of $200 million represent the largest donation in the institution’s history. When Ken took over, NYU was ranked number 54 in the nation. Today, it’s second behind the Mayo Clinic, ahead of all others.

I’ve known Ken since 1976. I met him with Doc Drelles at Pittsburgh National and knew immediately that he was a force. And then Ken hired Bob Grossman, another great leader, which made the management of NYU even stronger. And it’s the same thing in the equity business. You must find a leader in the right area and stick with them. Many philanthropists, when they give to something and it succeeds, walk away and move on to the next project. I look at a philanthropic effort more like a stock. Every time there’s a pullback, or a new opportunity, the answer is to back a great leader and trust them to make the right call.

Now, I don’t get into the philosophy of giving back. I give for selfish reasons. I love taking the money I’ve made and changing outcomes for people who haven’t had the opportunities that I’ve had. It’s fun. It’s a privilege. And I’m very proud of our record in philanthropy. I would not be happy if I spent a lot of money on something that didn’t move the needle.

I’m at the office very early in the morning until 5:30 p.m. every day, doing my job. And then I invest another 15 hours per week in philanthropy. In addition, my wife and I have raised three daughters and have four grandkids now, with probably more on the way. So, I have had a lot of luck in my life, but I can’t imagine myself ever retiring. I like what I do too much. And I think I’ll do it into my 90s, if I’m still around.

I have not been to Pittsburgh much lately, even though my firm’s headquarters and back office are there. When I first came to the city, it was still very blue-collar. Carnegie Mellon had not yet been built and drawn in high-tech business. But I always loved the people. They were friendly and down-to-earth. They were real. I love the fact that you can live in the country — and I don’t mean the suburbs — and be only 15 minutes from Downtown. And I love the relationship between the communities and their sports teams. I was there in ’79, when the Pirates won the World Series, and the Steelers won the Super Bowl in January 1980. I was 26, from nowhere, without a pot to pee in, but Pittsburgh welcomed me into “the club.”

When I lived in Pittsburgh, it was voted the nation’s “Most Livable City” two years in a row, and no one in other U.S. cities could believe it. Why? Because they had never been there. It was no longer the smoky city that it had been in the days when the steel mills were ablaze 24/7. And it’s still amazing to drive through that tunnel and see the “Golden Triangle” emerge, buildings sparkling in the sunshine. I always loved everything about Pittsburgh — and still do. I left only because I had to leave for business.

During my life, I’ve moved from here to there, all over the place, and consequently, never really had a home, per se. But to this day, even though I didn’t move to Pittsburgh until I was in my early 20s, and was only there physically for 12 years, I still consider it my hometown.

Jeff is an award-winning independent filmmaker and writer who specializes in defining the cultural significance of American people, places, things and events.