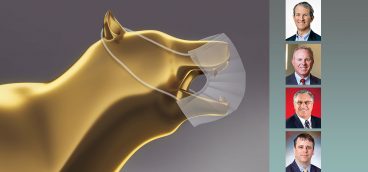

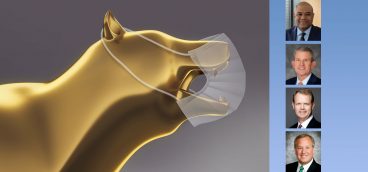

Positioning Client Portfolios: Wentling Tarquinio Loughney, Greycourt & Co, Henry Armstrong Associates

Each year in the summer issue, we ask a group of Pittsburgh’s leading investment experts to answer a question for our readers in 250 words or less. This year’s question: “The coronavirus has led to the first bear market in more than a decade with widespread uncertainty remaining. How are you positioning your client portfolios in this fraught environment?”

Thomas L. Wentling Jr., Wentling Tarquinio Loughney Wealth Consulting Group, UBS Financial Services Inc.

“Only when the tide goes out do you discover who’s been swimming naked.” —Warren Buffet. The survival manual for times like these requires that long before the onset of calamity, a continuous financial planning process has led to allocating resources to three buckets: Liquidity—one to three years of spending needs (individual circumstances); Longevity—balanced investment mix appropriate for remaining single/joint life expectancy; Legacy—longest time horizon and therefore most aggressive investment mix, within a client’s personal risk tolerance (we’re all different). If a plan like this is in place, it is far easier to withstand the “slings and arrows of outrageous fortune” (Hamlet, Act III, Scene I) and “be,” rather than “not to be.”

If, for any number of reasons, you never got around to the “dreaded” financial planning project, and here you are without sufficient liquidity—what to do? Wishing the market back up is not the answer. All roads always lead back to a plan. Find an advisor you trust and lay out your needs, wants and wishes. Her or his job is to help you assess which of those goals are possible given today’s reality, not what February made seem possible. The good news is that the Monte Carlo projections your planner will run will likely be more accurate about future market values now, as a lot of the air has come out of the tires since February. Within the confines of liquidity, longevity and legacy, taking life expectancy into account, a broadly diversified strategy is always the best bet.

Greg Curtis, Greycourt & Co.

We are expecting a U-shaped recovery, as opposed to a quick, V-shaped recovery or the dreaded L-shaped recovery. In other words, we think people will go back to work and will begin patronizing restaurants, bars and other non-essential items more or less as they did in the past, but that it will happen over a period of several quarters, not immediately. Thus, we believe the U.S. economy will be in recession through this year and into early 2021 but that the economy will gradually recover over next year. As a result, we are maintaining client positioning at or near the bottom of their risk ranges, rebalancing as necessary to avoid portfolios losing too much octane. We are being opportunistic in adding to equities where pricing has become extremely attractive, although we don’t believe prices are attractive across the board. For clients who panicked and sold out near the March bottom, we are establishing programs to get them reinvested over the balance of this calendar year.

James Armstrong, Henry Armstrong Associates

Stock market data over the last century make it clear that the market is a cyclical beast. Bears and bulls have finite lifespans, and follow each other inevitably (though unpredictably). We have believed for some time that the bull market that began in 2009 was getting long in the tooth, though we made no prediction as to exactly when, or why, it would end. We have been especially cautious for the last couple of years, and always try to hold portfolios of strong companies that could survive the next bear market or recession. We’ve generally avoided cyclical companies that are dependent upon large amounts of borrowed money, commodity-based companies such as oil, and companies whose stocks are very highly priced, as if a bear market or recession would never come.

The most recent “bear market” has been so short (only two months before its big upward bounce) that we don’t believe that a new bull market has yet begun. We also believe that the economic carnage inflicted by the coronavirus—38 million U.S. jobs lost in two months, and a collapse in demand for many sectors—energy, aviation, retail, travel & hospitality, among others—will eventually be reflected in lower stock prices.

Therefore, we see value in holding cash reserves to be used opportunistically if indeed stock prices fall again, and to ensure that client needs for cash can be met without having to sell stocks at bear-market prices when one arrives. We are battening down the hatches to prepare our investors, in the belief that it may take years, not months, for the global economy to fully recover.

Questions or corrections? Contact us at web@pittsburghquarterly.com.